Statement of Account — Per-Customer Receivables

A statement of account (SOA) is a single-page summary of every open invoice and recent payment for one customer. It is not a bill — it's a summary — and that distinction matters because customers treat the two very differently. A bill asks for action. A statement provides clarity. Send the right one at the right time and customers pay you on a more predictable schedule; mix them up and you end up with confused customers and a longer wait to get paid.

When you'd use this

- Month-end, sent automatically to every account with an open balance. This is the standard cadence.

- Mid-month, when a customer asks "what do I owe you?" — give them a statement, not a verbal answer.

- When following up on aging items, attach the statement to the email so the customer can see all open invoices in one place.

- When a customer requests records for their bookkeeper or auditor, the statement is what they want.

- As a polite collections nudge — "here's where things stand" lands more softly than "you're late."

You generally would not send a statement to a customer with no open balance. They'll wonder why you sent it. Some businesses send "zero-balance" statements monthly anyway as a service touch; that's a style choice. Most don't.

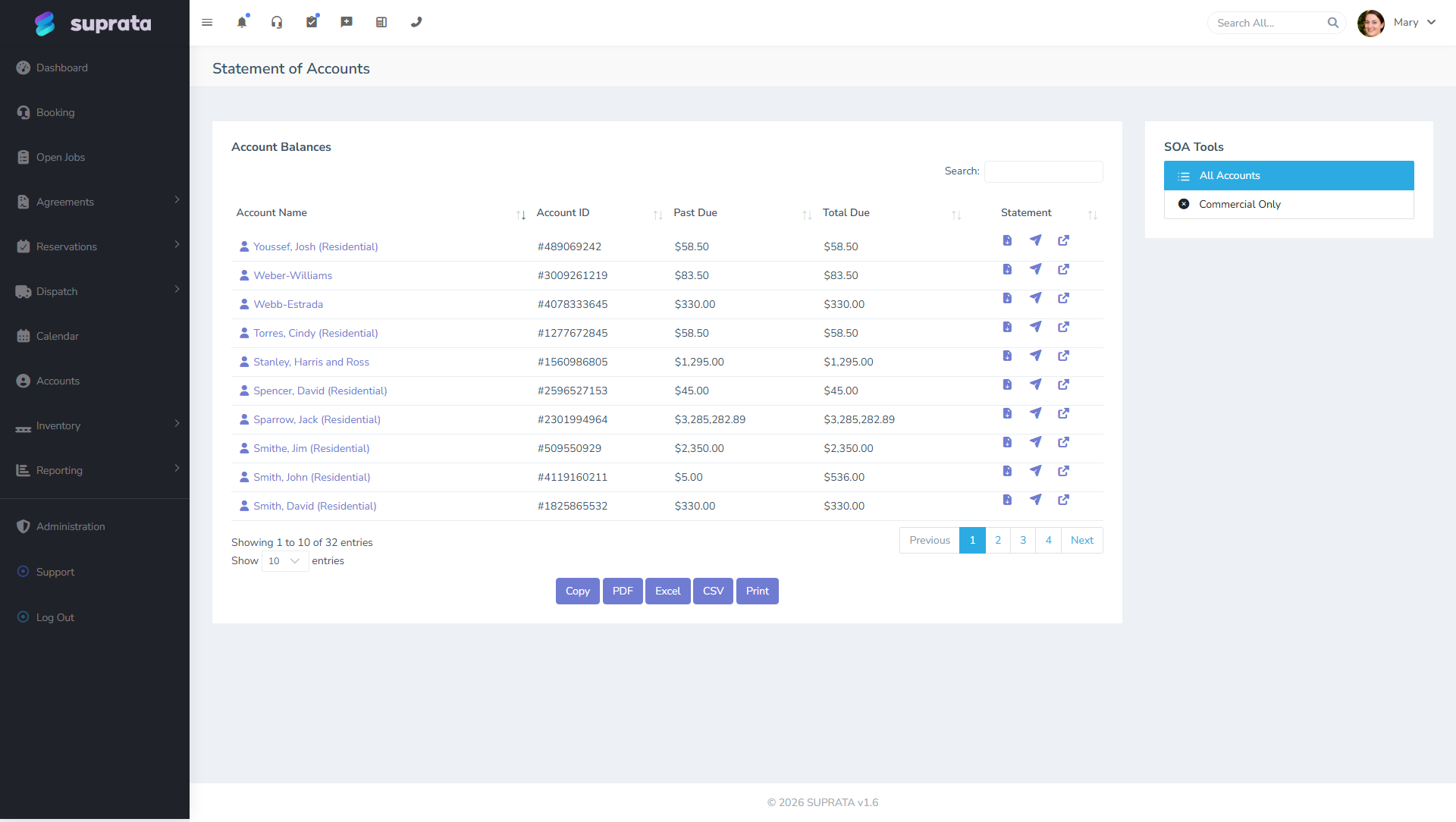

What's on a statement

A useful SOA includes:

- The customer's contact info and account number.

- A list of open (unpaid or partially paid) invoices, with date, invoice number, original amount, and remaining balance.

- Recent payments applied (so the customer can see you've credited what they sent).

- The aging breakdown — current, 1–30, 31–60, 61–90, 90+ — with totals per bucket.

- A grand total owed.

- Your remit-to address and payment instructions, including the link to pay online if you accept that.

That's it. A statement should not include unrelated marketing, multiple page styles, or a wall of fine print. The customer is looking for one number — what they owe — and a way to pay it.

How customers actually read it

Different audiences read the statement differently:

- The customer themselves wants to confirm two things: what's owed and whether you've credited recent payments. If they sent a check three weeks ago and don't see it, you'll get a phone call. Make sure recent payments are visible.

- Their bookkeeper wants to reconcile against their A/P. If the invoice numbers and amounts match what's in their system, they'll cut a check. If anything is off — wrong invoice number, wrong amount, missing PO reference — they'll kick it back and you'll lose a month.

- Their auditor, on the rare occasion, just wants paper. The statement satisfies that.

The implication: invoice numbering and amounts on the statement must match what was on the original invoice exactly. If you renumbered, voided-and-reissued, or merged invoices, expect questions.

How to send it

You have two paths:

- Email the PDF for routine month-end runs. This is the default for most customers.

- Print and mail for the small number of customers who don't email — typically older commercial accounts. Have a separate printed-statement workflow for these; don't try to make one process serve both.

Send statements on the same day every month — the 1st, the last business day, whatever — so customers learn to expect them. When the timing is predictable, customers pay on a predictable rhythm too.

What to do when a customer disputes the statement

Disputes happen. The customer says "I paid this," or "this invoice is wrong," or "we cancelled that order." Don't argue from the statement; argue from the underlying invoice and the payment record.

- Pull the specific invoice and look at its history.

- Check the payment list under their account — did anything come in that wasn't applied?

- If they show a payment you don't see, ask for the date and method. Bank ACH and check images usually resolve it in one call.

- If the dispute is about the work itself ("this wasn't done right"), it's not a statement question — it's a service question. Hand it off, don't try to resolve it on the collections call.

When to escalate from statement to demand letter

A statement is gentle. After two statements that don't move the needle, you've established a paper trail. The next step is a phone call from the owner; the step after that is a formal demand. Don't send statement after statement forever — they stop working after the second one if the customer was going to pay easily.

The right cadence for a slowly-aging account, in order:

- Month-end statement (routine).

- Second month, statement plus a personal note.

- Owner phone call (most accounts pay here).

- Formal demand letter with deadline.

- Collections agency or small-claims, depending on the dollar amount.

Common mistakes

- Treating a statement as a bill. Customers ignore statements they think they've already paid. A statement is a summary. The original invoice is the bill. Don't expect a statement alone to drive payment from a customer who didn't pay the invoice.

- Sending statements to current accounts. Confuses customers and trains them to ignore statements. Statements should only go to accounts with open balances unless you've made a deliberate choice to send zero-balance statements as a service touch.

- Inconsistent timing. If statements arrive on the 3rd one month and the 27th the next, customers don't know when to expect them and don't pay on a schedule. Pick a day and stick to it.

- Not including a payment link. If you accept online payments, the statement should have a way to pay right on it. Adding a "Pay Now" link is one of the easiest things you can do to get paid faster — every extra step between "I owe this" and "let me pay it" is a chance for the customer to put it down and forget.

- Letting voided invoices appear as open balances. Periodically reconcile voided and cancelled invoices so they don't keep showing up on statements. A statement showing $2,000 owed when half of that is from a voided estimate looks like an error to the customer — and it is.

- Sending statements without first checking the aging report. The aging report tells you who should receive a statement. Sending blanket statements wastes paper and trains customers to ignore them.

Related articles

- Reading the Billing & Sales Report

- The aging report — who to chase first

- Sending an invoice to a customer

- (Once "Writing off bad debt" is written, link to it here.)